鹰派信号惹众说纷纭:日本央行将再次加息?

日元汇率疲弱之际,在日本央行放出鹰派信号后,市场对于央行即将再次加息的猜测加剧。

近期,市场对于日本央行加息的猜测众说纷纭。在此日元汇率疲弱之际,部分分析师认为,央行很可能会通过调整债券收益率来防止日元继续贬值。

今年3月,日本央行结束了全球仅剩的负利率政策,并宣布将保持宽松的金融环境,并逐步提高利率。上周,日本央行将剩余5到10年到期的政府债券购买额削减了500亿日元(约合3.2亿美元),至4,250亿日元(约合27亿美元)。然而,十年期日本政府债券收益率保持相对平稳。

尽管日本政府曾两次即将出马干预以提振货币,并减少了对国债的购买力度,但日元仍处于市场几十年来的低位。与此同时,美联储官员认为今年降息次数将远少于市场预期的六次,而只会进行三次。

眼下,在日元疲软推动物价上涨之际,加上一系列因素的影响,日本提前加息的可能性增加。

5月8日,日本央行行长植田和男(Kazuo Ueda)在东京的一次活动上表示,如果通胀速度超出预期,央行将会提前调整利率,这一言论也与4月货币政策会议上的央行理事们的发言一致。

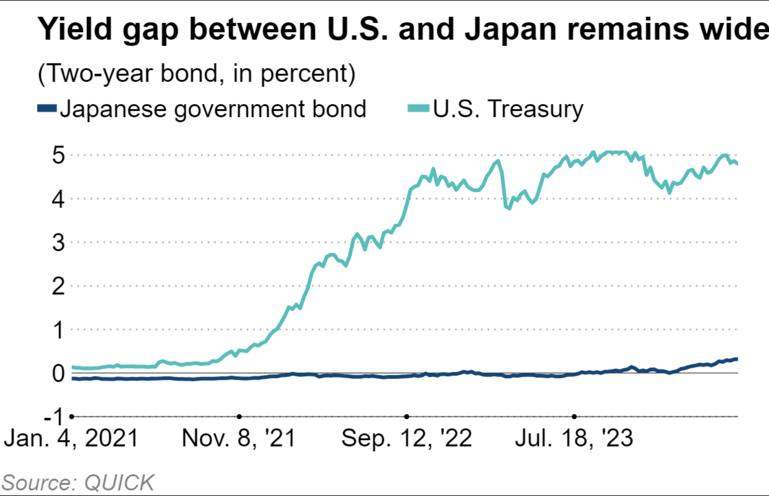

根据FactSet的数据,两年期日本国债的收益率为0.32%,这使得该债券对央行的利率调整非常敏感。这也意味着政策利率预计将在2024年下半年达到0.25%,次年达到0.5%。

瑞银证券首席日本经济学家、前日本央行官员安达正道(Masamichi Adachi)表示,4月25日至26日的货币政策上,植田行长的最新讲话和诸位官员的发言暗示了政府的鹰派立场,并强调日元的贬值很可能推高核心通胀。

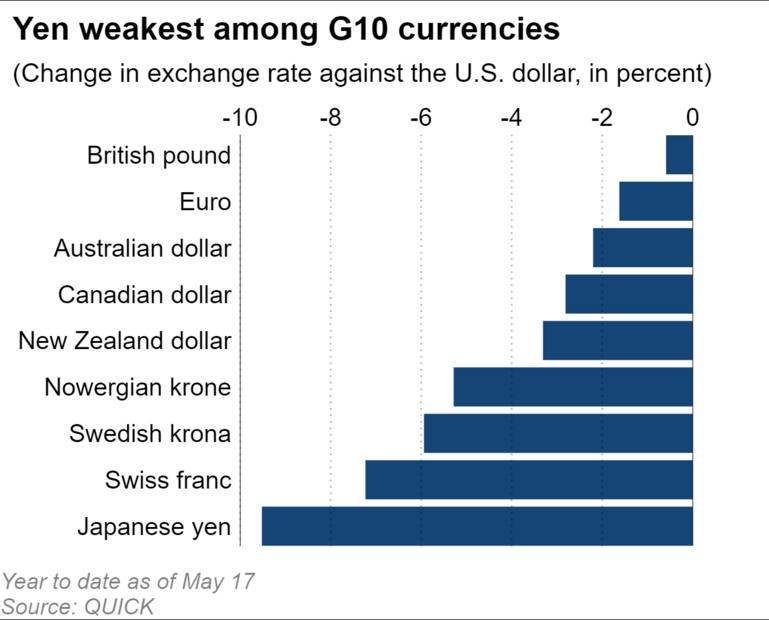

根据政府数据,日本核心消费者价格指数上涨了2.6%,略低于上个月的数据。5月17日,日元对美元的汇率维持在155水平,今年以来已下跌近10%,成为十国集团中表现最差的货币。

根据上周发布的初步数据,由于通胀超过工资增长,导致今年1月至3月消费下降,这也是连续第四个季度下降。摩根大通证券经济学家表示,“随着资本外流和通胀风险加剧,日本央行可能会面临催促利率调整的压力。

美银证券经济学家认为,除非日元跌破165,否则日本央行需要更多数据证明才会考虑加息举措,这样,政策制定者就可以以基础通胀加快为理由,而不单单考虑外汇因素。早前一份报告显示,美银证券已将下次加息至0.25%的预期时间从9月提前至7月,并预计明年1月将加息至0.5%,第二季度达0.75%。

上周,日本央行公开了一则人事变动,新任命了一位具有制定货币政策经验的执行理事,该变动也让市场对于央行的加息举动更加坚定。

不过,野村证券首席策略师松沢那夸(Naka Matsuzawa)等人预计,日本央行将仍然维持利率稳定,并逐渐发展至中性利率。他表示:“鉴于实际工资下降、经济信心下滑的情况,人们对央行加息的预测并无把握。实际上,民众更希望提高长期债券收益率,使收益率曲线更加陡峭,以阻止日元的进一步贬值。”

而实际上,日元的疲软源于美日之间巨大的利率差异,日元的走势也表明了其对美国的经济数据更为敏感的特点。

5月16日,随着美国4月份的消费者通胀数据和零售销售数据显示经济降温后,尽管日本一季度经济增长低于预期,且经济并未处于适合升息的最佳状态,但日元仍上涨至153水平。

瑞银证券的安达道通(Adachi)提到:“日元贬值的关键原因不在日本,而在美国。”因为美国利率创下了23年来的最高点,达到5.25%至5.50%。他表示:“在我们看来,日本央行可能不会在今年年底之前将利率提高到0.5%以上,这意味着如果美联储不降息,利率差异不会有明显的缩小。

·原创文章

免责声明:本文观点来自原作者,不代表Hawk Insight的观点和立场。文章内容仅供参考、交流、学习,不构成投资建议。如涉及版权问题,请联系我们删除。