美联储9月利率决议:超预期降息到来 政策出现重大拐点

央行的工作重心已经从“抗通胀”转换到“保就业”,未来市场的逻辑也会发生改变。

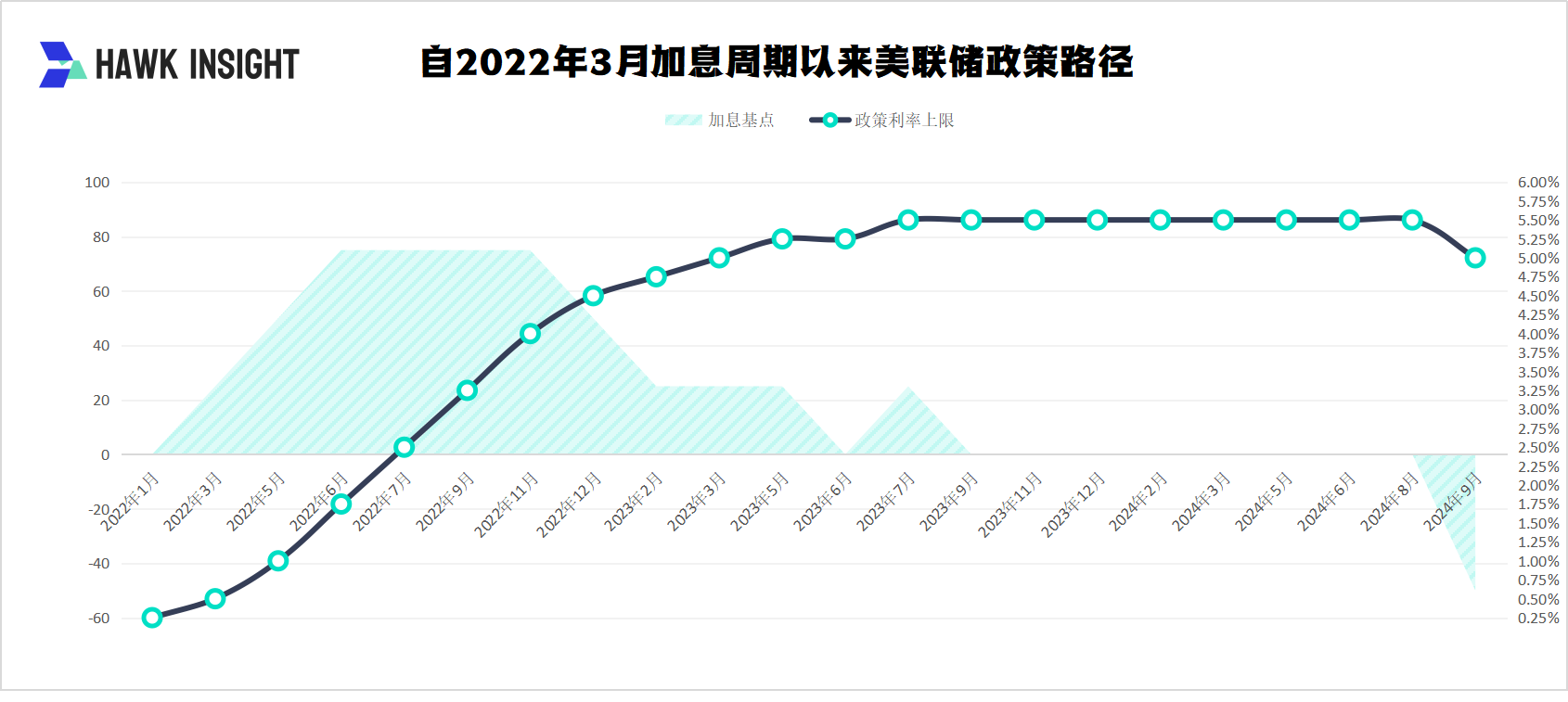

9月18日,靴子落地,美联储正式开启降息周期。根据FOMC利率决议,9月,美联储一次性降息50基点,超出市场预期,将政策利率区间拉低至4.75%-5.00%水平。

随后公布的SEP点阵图还显示,美联储年内还会有两次降息,每次25基点(或一次50基点的降息),年底的政策利率在4.25%-4.5%左右。

美联储政策逻辑已经改变

比决议结果更精彩的是决议内容。

对于通胀,美联储称:对通胀持续降至2%更有信心(has gained greater confidence)。

对于就业,美联储则称,就业增速“已放缓”(have slowed),失业率有所上升但仍保持低位;“委员会坚定致力于”新增“支持充分就业”(supporting maximum employment),与“将通胀率恢复到2%的目标”并列,且将就业目标前置。

美联储还宣布,实现就业和通胀双重目标的风险“大致平衡”(roughly in balance),代表政策逻辑已经发生变化,拐点随之到来。

分析称,从风险管理的平衡上来看,美联储目前显然是倒向了增长风险,即失业率的上升更令联储担心,而非通胀风险(包括二次通胀风险)。虽然8月的通胀数据中住房和核心通胀出现了一些负面变化,但不足以撼动联储目前的软着陆假设,二次通胀没有发生之前,分析师认为也没必要过早担心。

美联储在“保持物价稳定”和“保持充分就业”的双重目标中,继续迈进。

本次决议的另一个看点是票委的激辩。

首先是自2005年9月以来,第一次有票委对利率决议投了反对票:美联储理事米歇尔·W·鲍曼,她倾向于在本次会议上降息25个基点,而非50个基点。值得一提的是,鲍曼历来就是美联储最鹰派的发言人之一,她曾一直呼吁,通胀前景存在多重上行风险,太早或太快下调政策利率“都可能导致通胀反弹”。

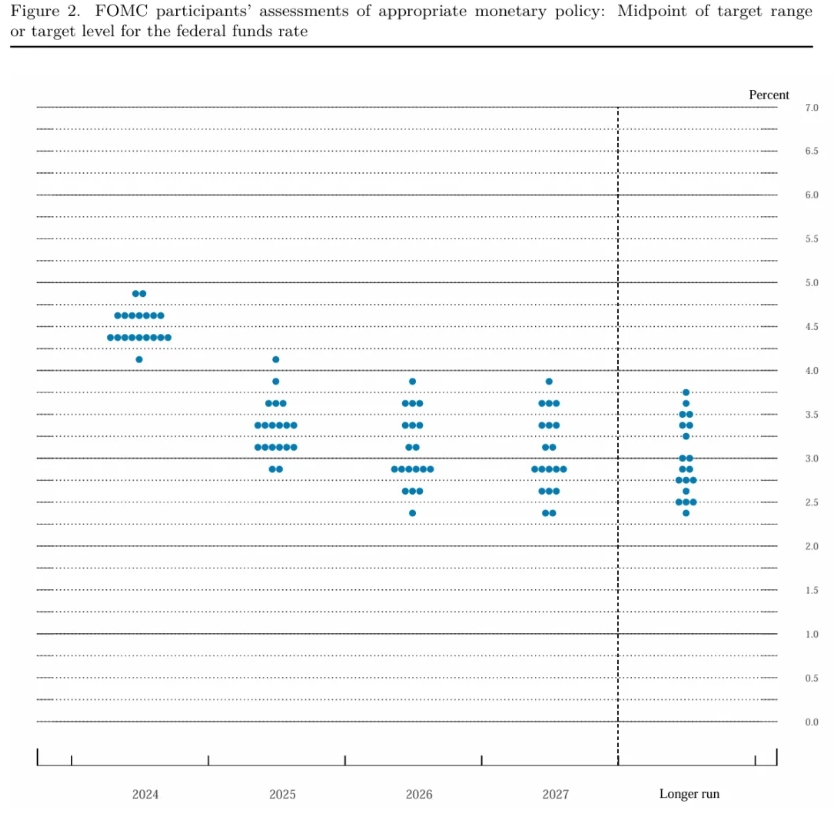

其次是异常激烈的点阵图。美联储预计今年还会降息50基点,不过形势较为焦灼:10位官员预计2024年降息100个基点或更多,9位官员预计2024年降息幅度为75个基点或更低。可以预见的是,未来两队人马会随着经济数据的出炉反复拉锯。

SEP经济预测摘要还称,预计2024年失业率为4.4%,6月料为4.0%;预计美国2024年GDP增速为2.0%,6月料为2.1%;预计2024年核心PCE通胀为2.6%,6月料为2.8%;预计2024年PCE通胀为2.3%,6月料为2.6%。

美元计价资产大幅波动 美股高位回落

利率决议公布后,受超预期降息提振,美股,美债,黄金应声上扬。

标普500指数盘中一度涨幅拉升至约1%,道指涨约375点,纳指100涨超1.1%;10年期美债收益率从3.69%上方跳水至3.64%下方,日内整体转跌。两年期美债收益率从3.64%上方跳水至3.54%下方;金价短线上扬大约20美元,报2,587.57美元/盎司,逼近9月16日所创历史最高位2,589.70美元。现货黄金持续走高,站上2,590美元/盎司关口,创历史新高,日内涨超0.7%。

美元一度走低:美元指数走低40点。英镑兑美元涨至1.3287,创2022年3月以来新高。

但是,随着鲍威尔在新闻发布会给出鹰派预期,叠加超预期降息引起人们对美国经济前景的担忧,声明公布后约13分钟,美股几乎回吐所有利率声明刚公布后的涨幅,美债收益率也明显收窄。

鲍威尔表示,SEP经济预测只是一个重新调校(“recalibration”)官员政策立场的过程,希望大家不要过度解读。SEP中没有任何迹象表明委员会急于求成(“no rush”)。调校的过程会随着时间的推移发生演变。我们可以加快步伐,我们可以放慢步伐,我们还可以暂停,这都视乎情况而定(“if appropriate”),但这正是我们要考虑的事情。

鲍威尔还称,所有人都不应当认为今天降息50个基点是新速度;美联储不会停止缩表,缩表可以和降息同时进行。他继续表示:“我个人的看法是,我们不会重返此前的低水平中性利率。”

截至收盘(新闻发布会结束后约40分钟),美股三大指数均收跌结束;现货黄金冲高回落,新闻发布会结束后刷新日低至2553.50美元,大幅低于新闻发布会开始后刷新的历史高位2600.16美元;ICE美元指数重返100.8上方。

目前的实际联邦基金利率并不真实

对于降息50个基点后的市场利弊,Yardeni Researc分析师表示,这能带来好处,包括可以为有需要的经济领域提供刺激、重振消费者和企业信心以及利好劳动力市场。住宅和商业地产(CRE)都将获得提振,CRE贷款将更容易获得再融资,从而降低该行业发生金融危机的风险。同时,宽松的货币政策有助于增加就业机会,从而控制失业率。

但是,降息50基点也会带来弊端,因为CPI中的服务业通胀粘性仍然较强,通胀仍有上行风险。不包括住房在内,8月服务业通胀同比上涨了4.3%。尤其是房租通胀的占比较大,这说明美联储宣布抗通胀“任务完成”为时过早。

另一方面,熟练劳动力可能会出现短缺。没有接受过高中教育的青少年是目前失业人数不断增加的原因,如果美联储过快降息,可能会产生两种结果:商品和服务需求增加,以及职位空缺增加。

最重要的是,目前的实际联邦基金利率并不真实。Yardeni Researc认为,美联储在14个月前就停止加息,代表其认为利率已经足以让通胀降至2.0%的目标。鲍威尔经常说,这个目标可以在不引发经济衰退的情况下实现。

而随着通胀下降,实际联邦基金利率正在上升,因此,美联储的货币政策将自动变得更具限制性,这在一定程度上或许会抵消降息的作用。

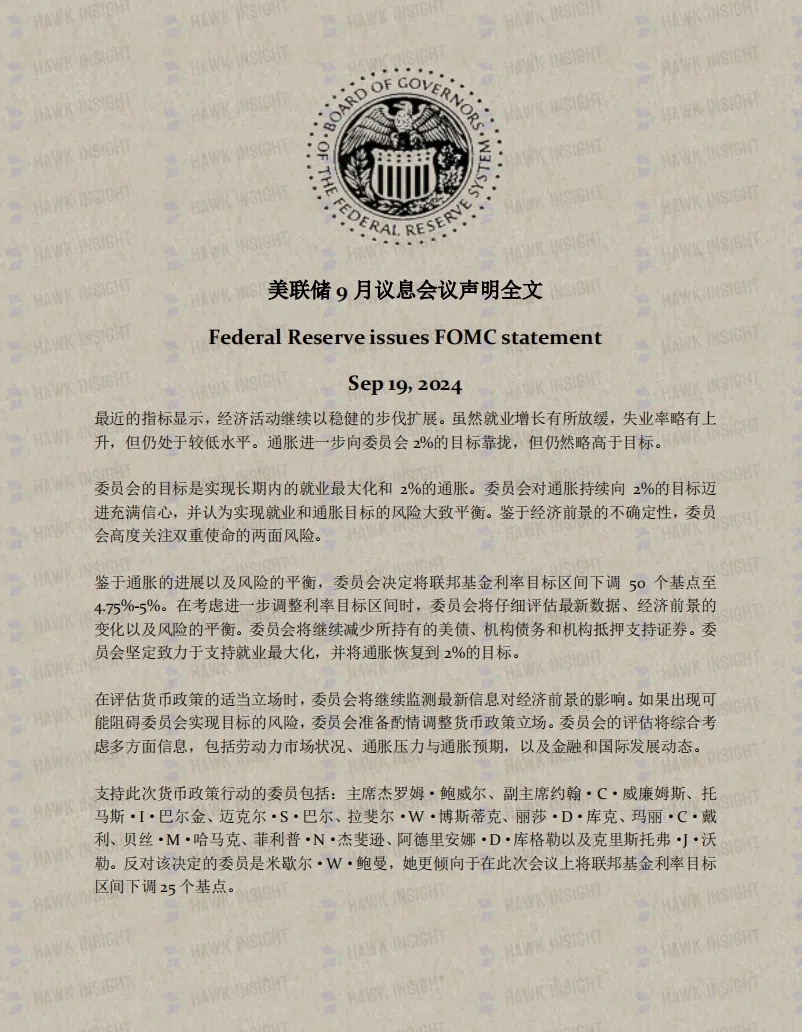

Hawk Insight附:美联储9月议息会议声明全文:

·原创文章

免责声明:本文观点来自原作者,不代表Hawk Insight的观点和立场。文章内容仅供参考、交流、学习,不构成投资建议。如涉及版权问题,请联系我们删除。